Bubble Alert! Is it Getting Too Easy to Get a Mortgage?

There is little doubt that it is easier to get a home mortgage today than it was last year. The Mortgage Credit Availability Index (MCAI), published by the Mortgage Bankers Association, shows that mortgage credit has become more available in each of the last several years. In fact, in June the last year:

-

More buyers are putting less than 20% down to purchase a home

-

The average credit score on closed mortgages is lower

-

More low-down-payment programs have been introduced

This has some people worrying that we are returning to the lax lending standards which led to the boom and bust that real estate experienced ten years ago. Let’s alleviate some of that concern.

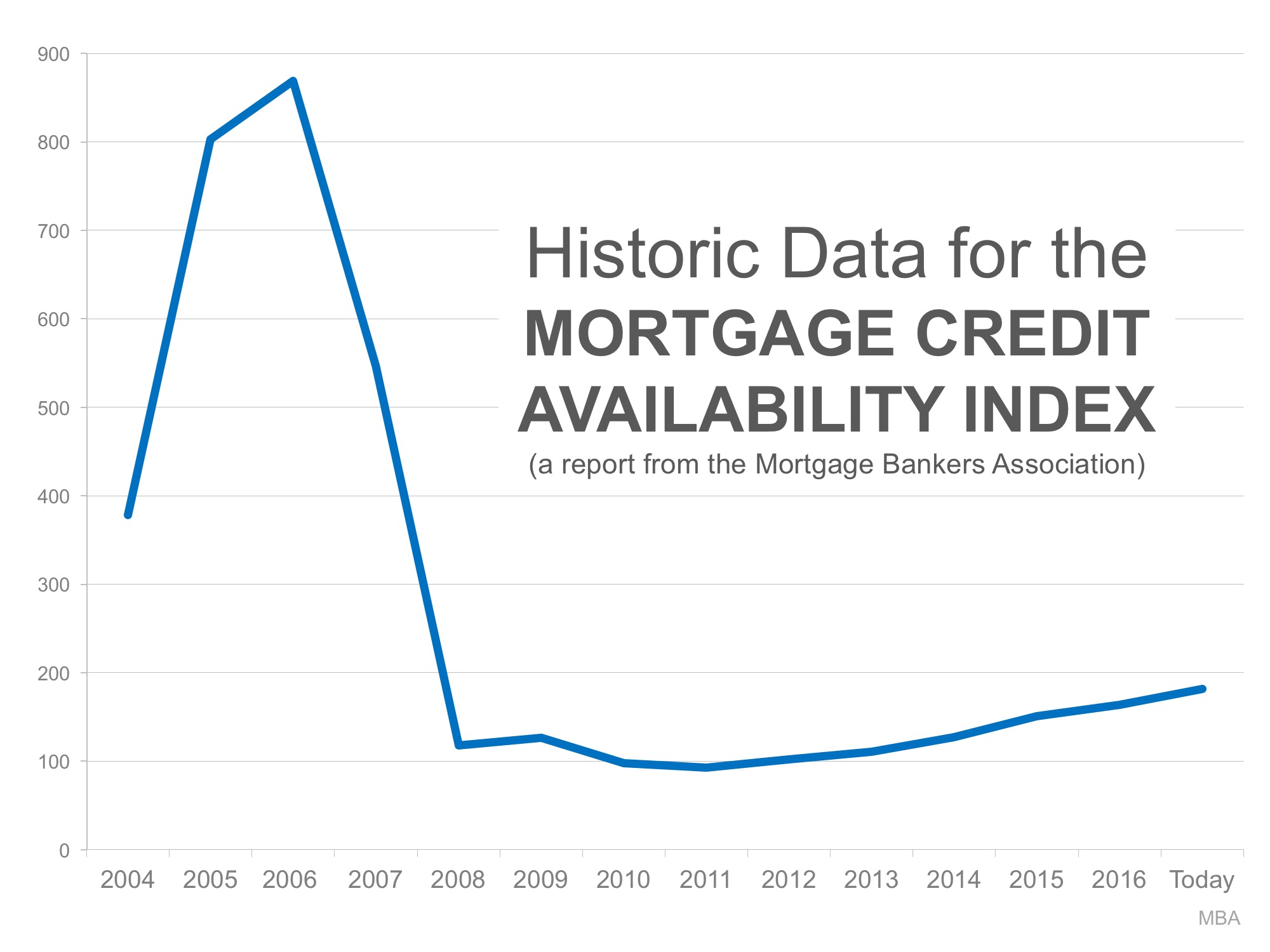

The graph below shows the MCAI going back to the boom years of 2004-2005. The higher the graph line, the easier it was to get a mortgage.

As you can see, lending standards were much more lenient from 2004 to 2007. Though it has gradually become easier to get a mortgage since 2011, we are nowhere near the lenient standards during the boom.

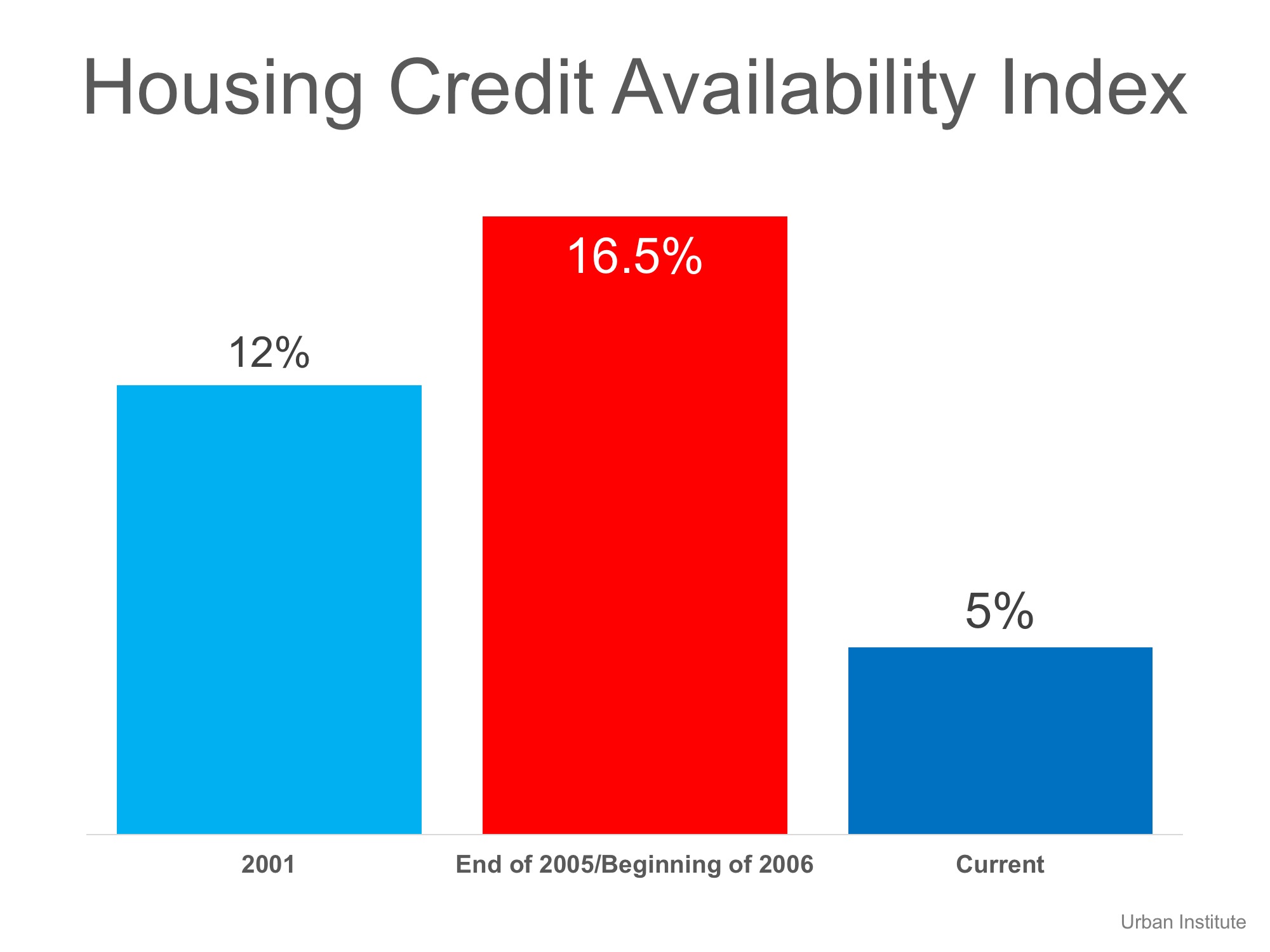

The Urban Institute also publishes a Home Credit Availability Index (HCAI). According to the institute, the HCAI:

“Measures the percentage of home purchase loans that are likely to default – that is, go unpaid for more than 90 days past their due date. A lower HCAI Indicated that lenders are unwilling to tolerate defaults and are imposing tighter lending standards, making it harder to get a loan. A higher HCAI indicates…it is easier to get a loan.”

Here is a graph showing their findings:

Again, today’s lending standards are nowhere near the levels of the boom years. As a matter of fact, they are more stringent than they were even before the boom.

Bottom Line

It is getting easier to gain financing for a home purchase. However, we are not seeing the irresponsible lending that caused the housing crisis.

To view original article, please visit Keeping Current Matters.

3 Graphs Showing Why You Should Sell Your House Now

If you’re thinking about moving, these three graphs clearly show that it’s a great time to sell your house.

4 Big Incentives for Homeowners to Sell Now

The key to continued success in the residential housing market is for more listings to come on the market. Are you ready to sell?

Americans Find the Nonfinancial Benefits of Homeownership Most Valuable

The non-financial side of homeownership is most valued after a year full of pandemic-driven challenges.

Patience Is the Key to Buying a Home This Year

Low inventory in the housing market isn’t new, but it’s becoming more challenging to navigate.

Will the Housing Market Maintain Its Momentum?

Experts have forecasted that total home sales (existing homes and new construction) will continue their momentum into next year.

4 Tips to Maximize the Sale of Your House

Despite the speed and opportunity for sellers, there are still steps you can take to prep your house so you get the greatest possible return.

Planning to Move? You Can Still Secure a Low Mortgage Rate on Your Next Home

To take advantage of today’s real estate market, experts are encouraging homeowners to act now before interest rates climb.

How Much Time Do You Need To Save for a Down Payment?

The national average for the time it would take to save for a 10% down payment is right around two and a half years (2.53).

93% of Americans Believe a Home Is a Better Investment Than Stocks

Housing represents the largest asset owned by most households and is a major means of wealth accumulation.

Some Buyers Prefer Smaller Homes

If your house is no longer the best fit for your evolving needs, it may be time to put your equity to work for you and downsize to the home you really want.