Bubble Alert! Is it Getting Too Easy to Get a Mortgage?

There is little doubt that it is easier to get a home mortgage today than it was last year. The Mortgage Credit Availability Index (MCAI), published by the Mortgage Bankers Association, shows that mortgage credit has become more available in each of the last several years. In fact, in June the last year:

-

More buyers are putting less than 20% down to purchase a home

-

The average credit score on closed mortgages is lower

-

More low-down-payment programs have been introduced

This has some people worrying that we are returning to the lax lending standards which led to the boom and bust that real estate experienced ten years ago. Let’s alleviate some of that concern.

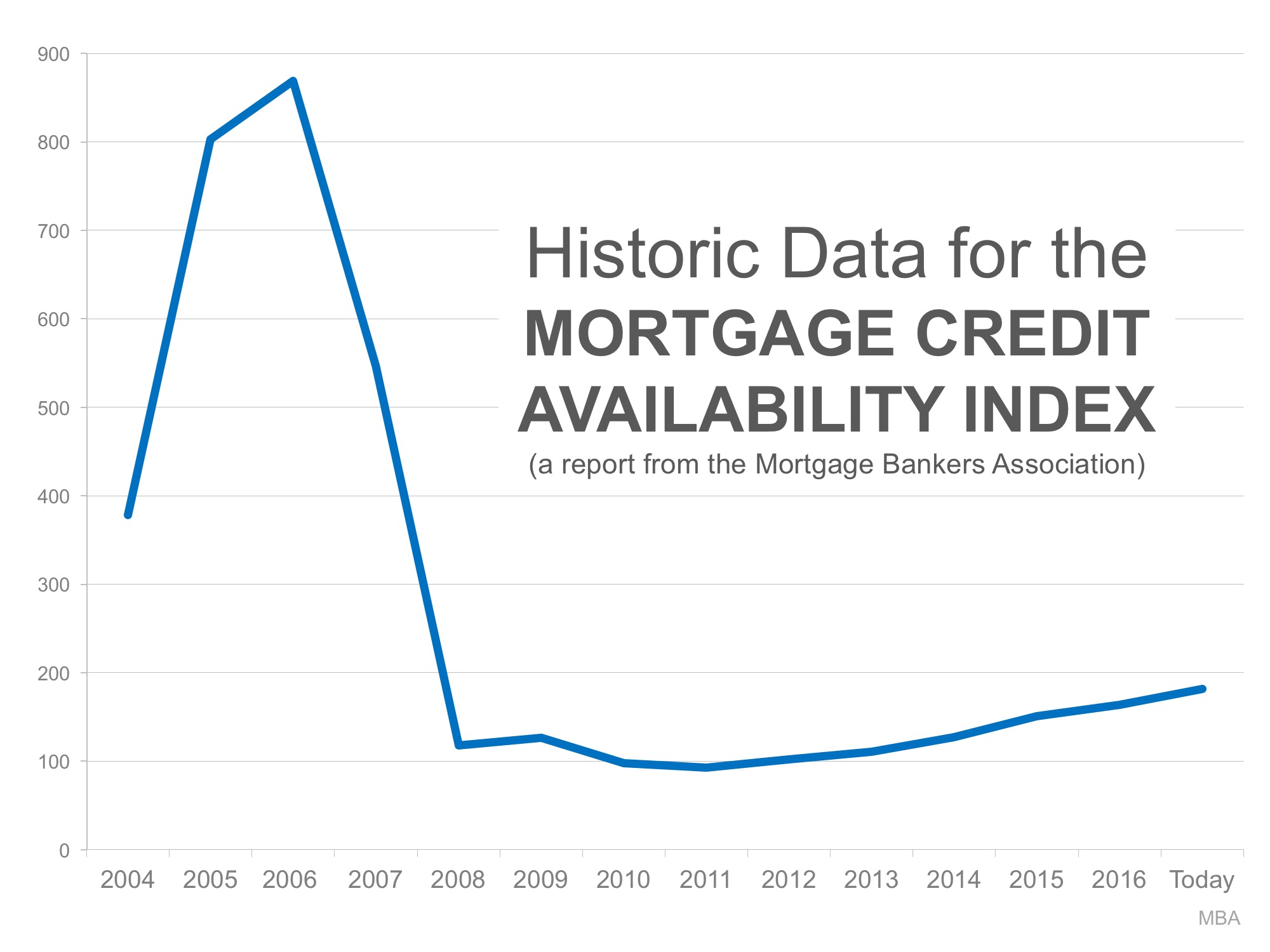

The graph below shows the MCAI going back to the boom years of 2004-2005. The higher the graph line, the easier it was to get a mortgage.

As you can see, lending standards were much more lenient from 2004 to 2007. Though it has gradually become easier to get a mortgage since 2011, we are nowhere near the lenient standards during the boom.

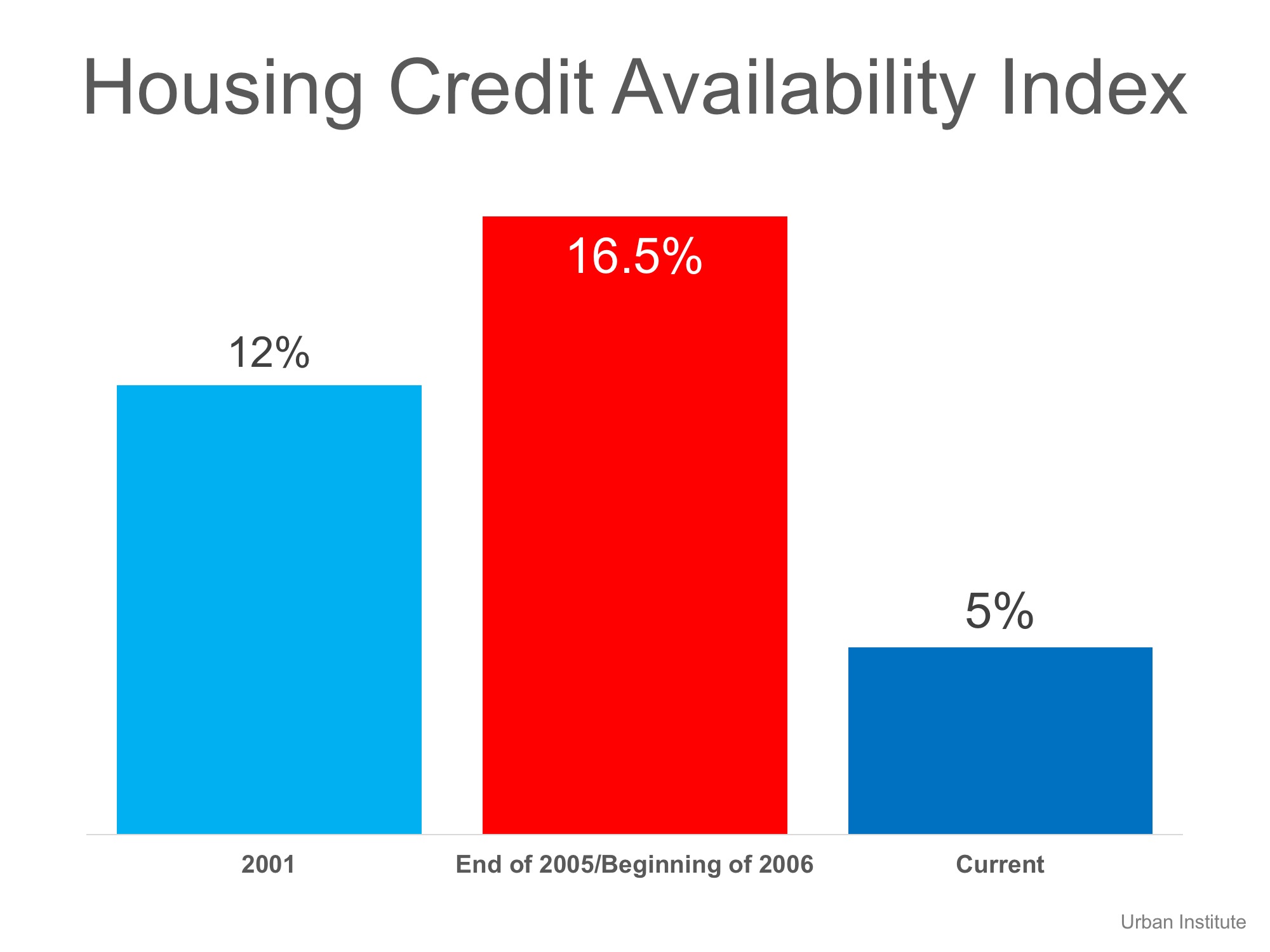

The Urban Institute also publishes a Home Credit Availability Index (HCAI). According to the institute, the HCAI:

“Measures the percentage of home purchase loans that are likely to default – that is, go unpaid for more than 90 days past their due date. A lower HCAI Indicated that lenders are unwilling to tolerate defaults and are imposing tighter lending standards, making it harder to get a loan. A higher HCAI indicates…it is easier to get a loan.”

Here is a graph showing their findings:

Again, today’s lending standards are nowhere near the levels of the boom years. As a matter of fact, they are more stringent than they were even before the boom.

Bottom Line

It is getting easier to gain financing for a home purchase. However, we are not seeing the irresponsible lending that caused the housing crisis.

To view original article, please visit Keeping Current Matters.

6 Foundational Benefits of Homeownership Today

As we think about the future and what we want to achieve beyond 2021, it’s a great time to look at the benefits of owning a home.

Do I Really Need a 20% Down Payment to Buy a Home?

Be sure to work with trusted professionals from the start to learn what you may qualify for in the homebuying process.

Why Owning a Home Is a Powerful Financial Decision

In today’s housing market, there are clear financial benefits to owning a home including the chance to build your net worth.

Want to Build Wealth? Buy a Home This Year.

A financial advantage to owning a home is the wealth built through equity when you own a home.

Turn to an Expert for the Best Advice, Not Perfect Advice

An agent can give you the best advice possible based on the information and situation at hand.

What Happens When Homeowners Leave Their Forbearance Plans?

If we do experience a higher foreclosure rate, most experts believe the current housing market will easily absorb the excess inventory.

What’s the Difference between an Appraisal and a Home Inspection?

Here’s the breakdown of each one and why they’re both important when buying a home.

Why Moving May Be Just the Boost You Need

There’s logic behind the idea that making a move could improve someone’s quality of life

Owning a Home Is Still More Affordable Than Renting One

In 2020, mortgage rates reached all-time lows 16 times, and so far, they’re continuing to hover in low territory this year.

Should I Wait for Lower Mortgage Interest Rates?

Borrowers are smart to take advantage of these low rates now and will certainly benefit as a result.