Homeowners: Your House Must Be Sold TWICE

In today’s housing market, where supply is very low and demand is very high, home values are increasing rapidly. Many experts are projecting the home values could appreciate by another 5%+ over the next twelve months. One major challenge in such a market is the bank appraisal.

If prices are surging, it is difficult for appraisers to find adequate, comparable sales (similar houses in the neighborhood that recently closed) to defend the selling price when performing the appraisal for the bank.

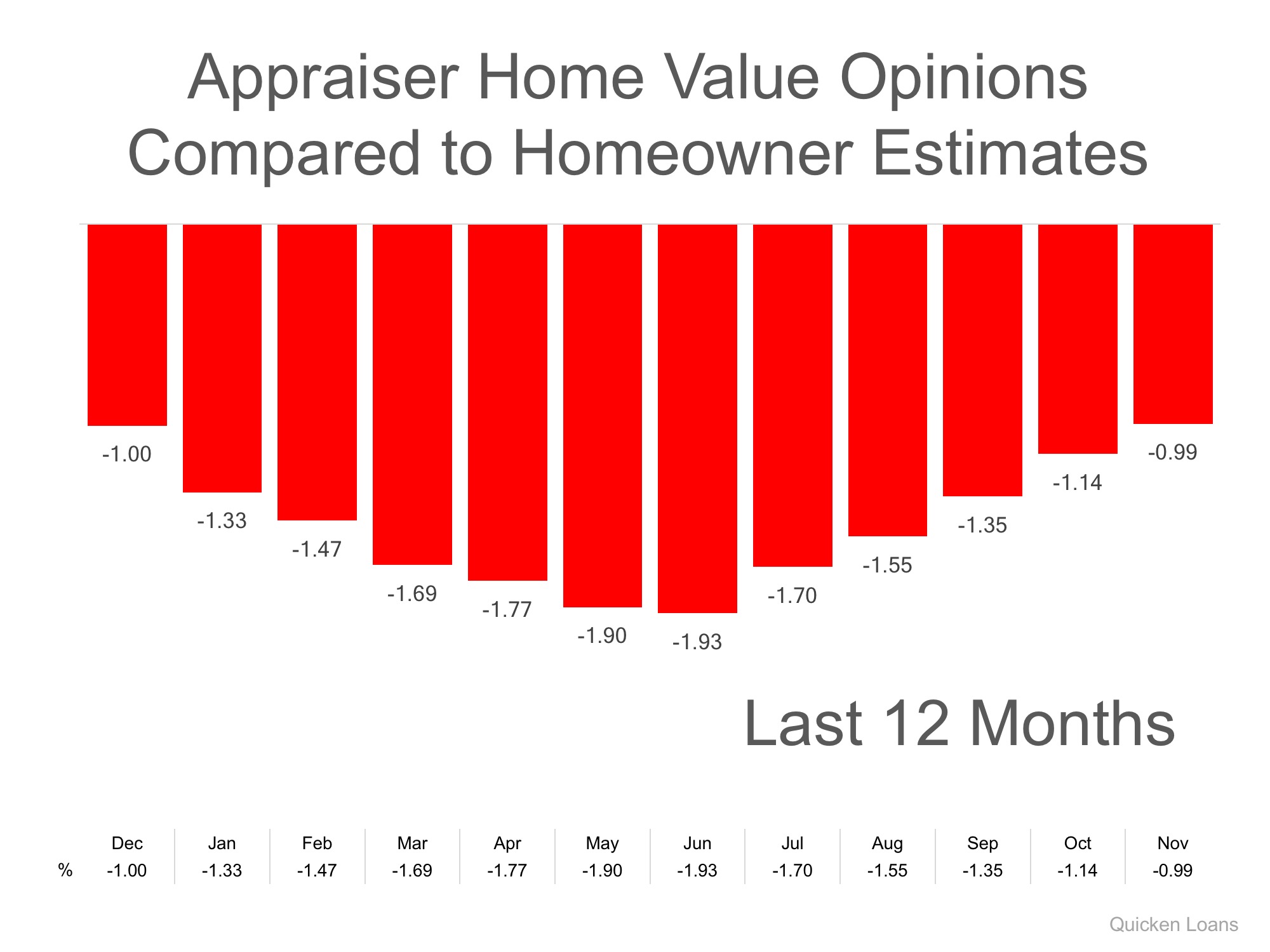

Every month in their Home Price Perception Index (HPPI), Quicken Loans measures the disparity between what a homeowner who is seeking to refinance their home believes their hose is worth, and an appraiser’s evaluation of that same home.

Bill Banfield, Executive VP of Capital Markets at Quicken Loans urges anyone looking to buy or sell in today’s market to remember the impact of this challenge:

“Based on the HPPI, it appears homeowners in the markets where prices are rising faster than the national average – like Denver, Seattle and San Francisco – are continuing to underestimate just how quickly home values are rising, so the average appraisal is higher than homeowner estimate.

On the inverse of that, homeowners in areas where the values aren’t rising as fast may think they are rising faster than they are, leading to the appraisal lagging the estimate.”

The chart below illustrates the changes in home price estimates over the last 12 months.

Bottom Line

Every house on the market must be sold twice; once to a prospective buyer and then to the bank (through the bank’s appraisal). With escalating prices, the second sale might be even more difficult than the first. If you are planning on entering the housing market this year, let’s get together to discuss this and any other obstacles that may arise.

To view original article, please visit Keeping Current Matters.

Homeownership Is Full of Financial Benefits

Does homeownership actually give you a better chance to build wealth?

Latest Jobs Report: What Does It Mean for You & the Housing Market?

With listing inventory down 52% from a year ago, bidding wars are skyrocketing. As a result, home prices are climbing.

Don’t Sell on Your Own Just Because It’s a Sellers’ Market

Real estate professionals are trained negotiators with a ton of housing market insights that average homeowners may never have.

Your Tax Refund and Stimulus Savings May Help You Achieve Homeownership This Year

Your tax refund may cover more of a down payment than you realize.

How a Change in Mortgage Rate Impacts Your Homebuying Budget

Anytime there’s a change in the mortgage rate, it affects what buyers can afford to borrow when buying a home.

What It Means To Be in a Sellers’ Market

Low mortgage rates and a year filled with unique changes have prompted buyers to think differently about where they live – and they’re taking action.

Buyer & Seller Perks in Today’s Housing Market

Buyers are clearly eager to purchase so homeowners who are in a position to sell shouldn’t wait to make their move!

Why You Should Think About Listing Prices Like an Auction’s Reserve Price

Frequent and competitive bidding wars are creating an auction-like atmosphere in many real estate transactions.

Should We Fear the Surge in Cash-Out Refinances?

Today’s cash-out refinance situation bears no resemblance to the situation that preceded the housing crash.

What Credit Score Do You Need for a Mortgage?

Planning to buy a home? Speak to an expert about steps you can take to improve your credit score so you’re in the best position possible.