"Many have begun to reexamine the idea of buying a home, choosing instead to rent for a while. What is the right choice for you?"

In a real estate market where home prices are rising, many have begun to reexamine the idea of buying a home, choosing instead, to rent for a while. But often, there is a dilemma: should you keep paying rent, knowing that rent is rising too, or should you lock in your housing cost and buy a home?

Let’s look at both scenarios and analyze the pros and cons of each:

Renting

With the housing market crash in 2008, many homeowners lost their homes and became renters. According to Iproperty Management, “the number of households renting their home … rose from 31.2% of households in 2006 to 36.6% in 2016”.

Some choose to rent because it is more convenient for their lifestyle. Those whose job requires frequent moves need the flexibility that a 6-12 month lease agreement gives them so they can move to their next assignment!

Many renters believe that renting is cheaper because they do not have to pay for maintenance and repairs. (Not true! Landlords work those expenses into your rent and other fees). Another reason many rent is that they feel like they cannot afford the down payment and closing costs required to buy a house, due to their inability to save much after paying their monthly expenses.

That can be true! Nearly 1 in 4 renters spend at least half their household income on rent. In 2017 the “severely” burdened renters’ rate was 24.7% with 24.9% reporting they were “moderately” burdened.

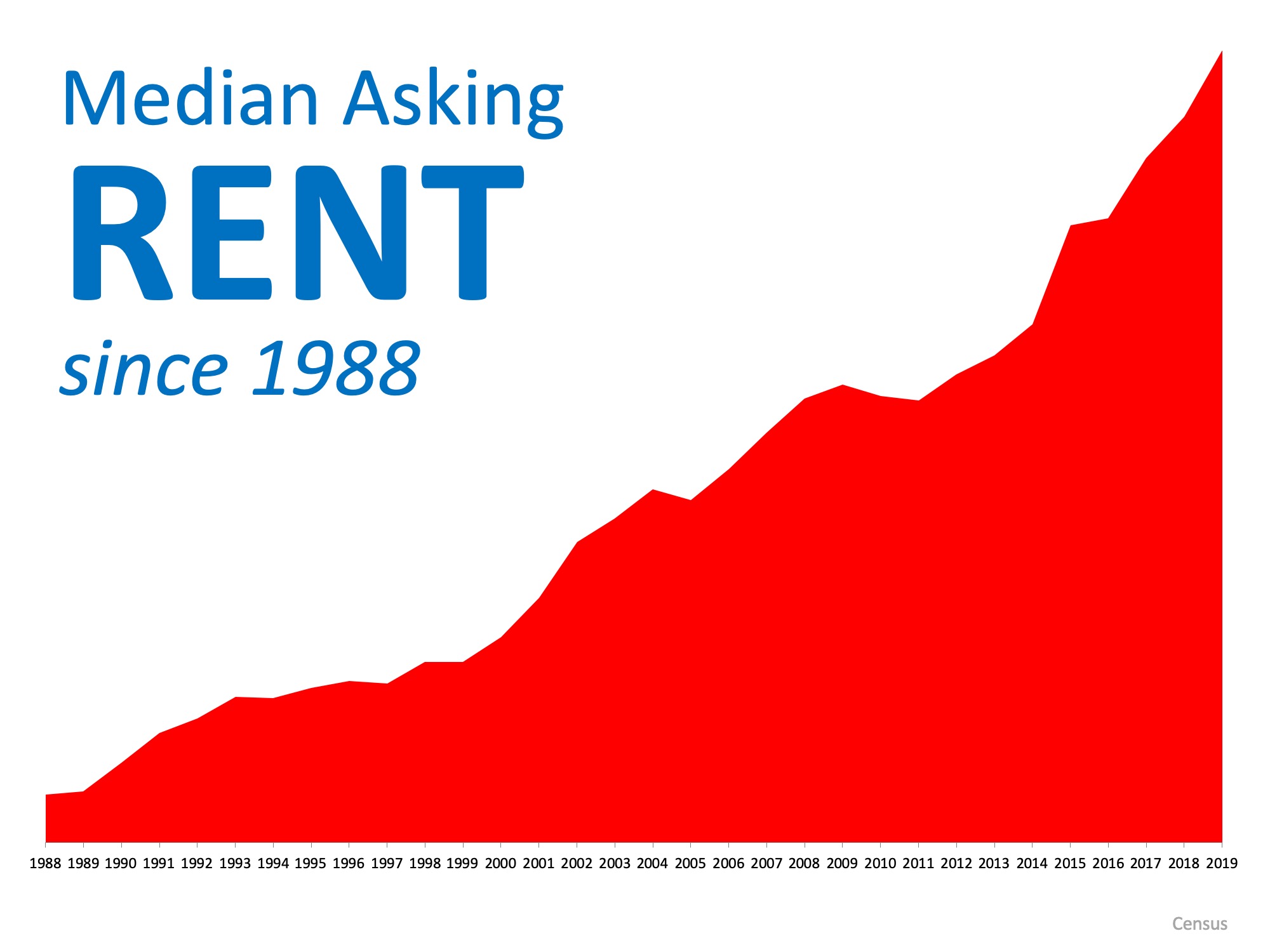

Renting also brings some financial disadvantages. Homeowners can take advantage of tax deductions that let them claim their property taxes and mortgage interest. Additionally, there is a big risk that your rent will go up every time you renew your lease, as we know the median asking rent has been increased steadily since 1988! One of the major challenges with renting is that you don’t have a space to call your own. When you rent, you are paying your landlord’s mortgage, and therefore they are the beneficiaries of the equity gained from paying that mortgage.

One of the major challenges with renting is that you don’t have a space to call your own. When you rent, you are paying your landlord’s mortgage, and therefore they are the beneficiaries of the equity gained from paying that mortgage.

Now let’s explore the other side: Homeownership

In the past, we have mentioned the many financial and non-financial benefits of becoming a homeowner. So, let’s just focus on the one big difference between renting and owning, the ability to lock in your housing cost!

Assuming you will have a fixed-rate mortgage, your costs are predictable! You will know exactly what your mortgage payment will be for the next 15-30 years. The homeownership rate in 2018 was 64.4%, and has been on the rise. Those households locked in their housing cost rather than wait for their landlord to raise their rent again!

What are the disadvantages of owning a home? Well, it is a long-term financial commitment! It is not easy to pack quickly and move. You will need time and good planning to do it in a short amount of time.

You need to save your money! Getting a mortgage requires a down payment, closing costs, and moving expenses. Again, that will require some savings and planning!

Unless you have a homeowner’s association (HOA) (and you pay an HOA fee) or a home warranty, you will be responsible for maintenance and taking care of the home. This may range anywhere from regular landscaping to major repairs.

Bottom Line

Like everything in life, there are pros and cons. What is better for you depends on your situation! If you are interested in becoming a homeowner and want to discuss the pros and cons, let’s get together to help you review your current situation and answer any questions you may have!

To view original article, visit Keeping Current Matters.

Why Staging Your House Could Pay Off This Spring

Staging doesn’t always have to mean hiring a full crew or filling your house with rented furniture. There are a few different paths you can take.

4 Ways To Give Your Offer an Edge This Spring

Here’s what you should know if you’re looking to buy a home during this busy spring season.

Rent or Buy? The Real Tradeoff Most People Don’t Talk About

Whether you’re looking to buy now or planning for the future, the first step is the same. Have a quick conversation with a local real estate agent about your goals, timeline, and budget.

The Best Week To List Your House Is Just Around the Corner

Based on analysis of historical trends, the ideal week to put your house on the market this year is: April 12–18.

Affordability Has Improved in All 50 States

When buyers have more choices, it creates a healthier balance in the market and that can help bring affordability back within reach.

The Remodel You’ve Been Dreaming About May Be Closer Than You Think

Whether the project you’ve been thinking about is on this list or not, chat with an agent to make sure it’s worth the time, money, and effort before calling in any contractors.