When you’re thinking about buying a home, your credit score is one of the biggest pieces of the puzzle. Think of it like your financial report card that lenders look at when trying to figure out if you qualify, and which home loan will work best for you. As the Mortgage Report says:

“Good credit scores communicate to lenders that you have a track record for properly managing your debts. For this reason, the higher your score, the better your chances of qualifying for a mortgage.”

The trouble is most buyers overestimate the minimum credit score they need to buy a home. According to a report from Fannie Mae, only 32% of consumers have a good idea of what lenders require. That means nearly 2 out of every 3 people don’t.

So, here’s a general ballpark to give you a rough idea. Experian says:

“The minimum credit score needed to buy a house can range from 500 to 700, but will ultimately depend on the type of mortgage loan you’re applying for and your lender. Most lenders require a minimum credit score of 620 to buy a house with a conventional mortgage.”

Basically, it varies. So, even if your credit isn’t perfect, there are still options out there. FICO explains:

“While many lenders use credit scores like FICO Scores to help them make lending decisions, each lender has its own strategy, including the level of risk it finds acceptable. There is no single “cutoff score” used by all lenders, and there are many additional factors that lenders may use . . .”

And if your credit score needs a little TLC, don’t worry—Experian says there are some easy steps you can take to give it a boost, including:

1. Pay Your Bills on Time

Lenders want to see that you can reliably pay your bills on time. This includes everything from credit cards to utilities and cell phone bills. Consistent, on-time payments show you’re a responsible borrower.

2. Pay Off Outstanding Debt

Paying down what you owe can help lower your overall debt and make you less of a risk to lenders. Plus, it improves your credit utilization ratio (how much credit you’re using compared to your total limit). A lower ratio means you’re more reliable to lenders.

3. Don’t Apply for Too Much Credit

While it might be tempting to open more credit cards to build your score, it’s best to hold off. Too many new credit applications can lead to hard inquiries on your report, which can temporarily lower your score.

Bottom Line

Your credit score is crucial when buying a home. Even if your score isn’t perfect, there are still pathways to homeownership.

Working with a trusted lender is the best way to get more information on how your credit score could factor into your home loan.

To view original article, visit Keeping Current Matters.

Are You Ready for the ‘Black Friday’ of Real Estate?

New realtor.com study reports the week of September 22 is the best time of year to buy a home, making it ‘Black Friday’ for homebuyers.

Should You Fix Your House Up or Sell Now?

If you’re considering selling your house, let’s get together to help you confidently determine what the best choice for you and your family is.

Is Your House “Priced to Sell Immediately”?

In today’s real estate market, more houses are coming to market every day. Pricing your home right from the start can make a big difference!

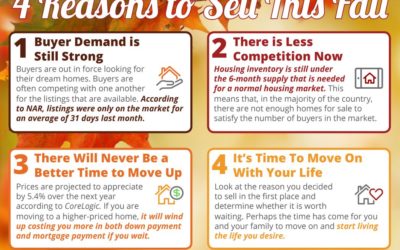

4 Reasons to Sell This Fall

Fall is a great time to sell your house! Take a look at 4 great reasons why you should consider selling this Fall and then let us help you with the rest!

What Buyers Need to Know About HOAs

It’s important to understand what fees, structures, and regulations will come into play if there is an HOA where you’d like to live. We can help you! Give us a call today!

One of the Top Reasons to Own a Home

One of the benefits of homeownership is that it is a “forced savings plan.” Tired of renting and paying into your landlord’s equity? Give #brookhamptonrealty a call today!