"A lot of first-time buyers are struggling to buy a home in today’s market."

If you’re a homeowner, chances are you’ve built up a lot of wealth – just by living in your house and watching its value grow over time. And that equity? It’s something that could help change your child’s life.

Since affordability is still a challenge, a lot of first-time buyers are struggling to buy a home in today’s market. Even if they have a stable job and a solid plan, buying can still feel out of reach. But that’s where your equity could make all the difference.

To give you an idea, the average homeowner with a mortgage has $311,000 worth of equity, according to Cotality (formerly CoreLogic). That’s significant. And some parents are using a portion of their equity to help their children become homeowners, too.

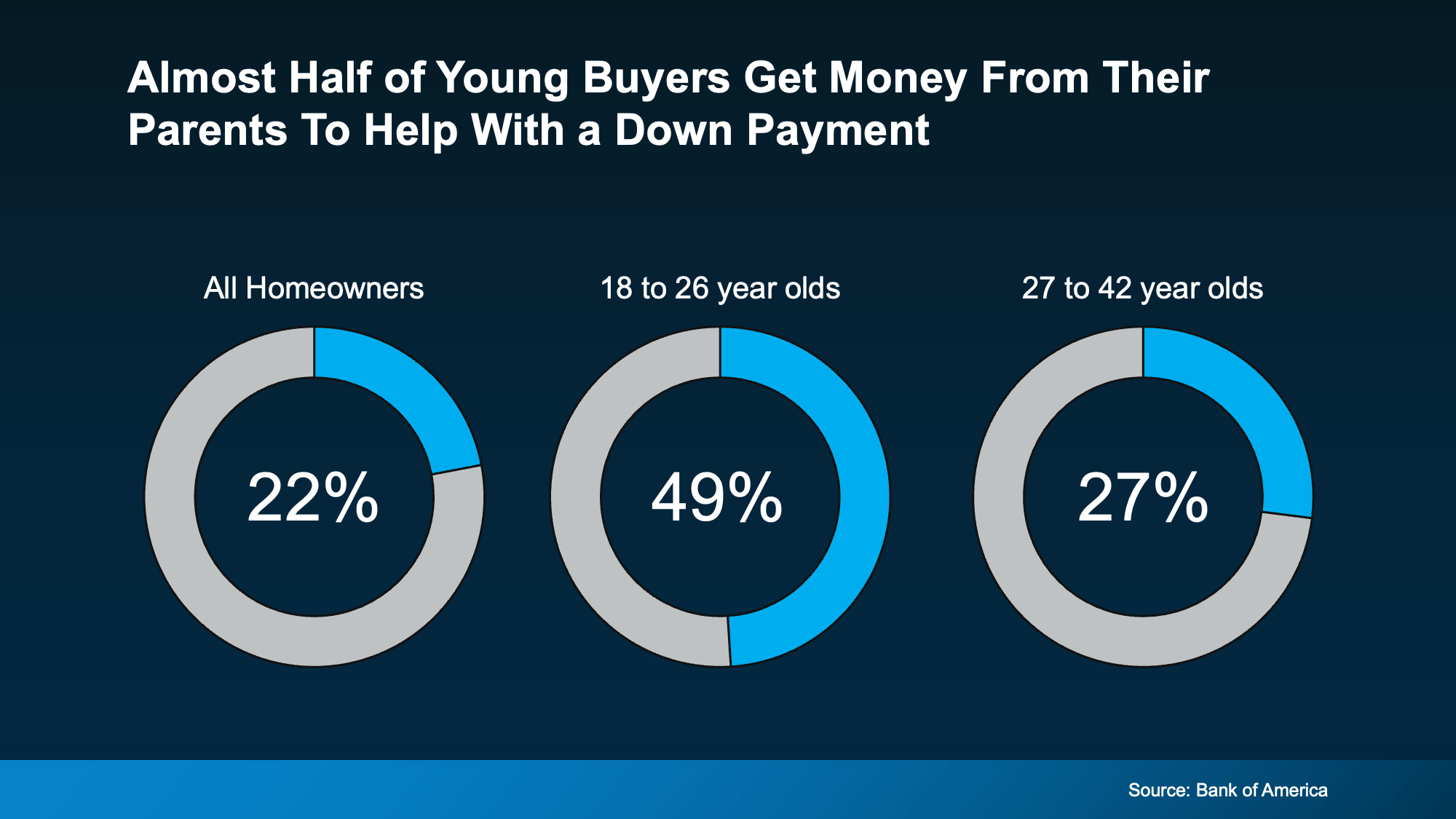

According to Bank of America, 49% of buyers between 18 and 26 got money from their parents to use toward their down payment (see chart below):

Even though the data doesn’t specify how many parents used their equity, the wealth they’ve built through homeownership may have helped make it possible – especially given how much equity the average homeowner has today.

Even though the data doesn’t specify how many parents used their equity, the wealth they’ve built through homeownership may have helped make it possible – especially given how much equity the average homeowner has today.

While what’s right for each person’s specific situation will vary on a case-by-case basis, that’s a powerful legacy to pass on. It helps those younger people buy a home, build equity of their own, and begin the next chapter of their life with a little less financial stress and a lot more stability. And for those parents? It’s a way to turn what they've built into something deeply meaningful.

This isn’t just about money. For many homeowners, it’s about being the reason their child gets to say, “we got the house.” And giving them the kind of head start they might’ve only dreamed of at their age. And here’s the part that really sticks. Compare the Market says:

“Of those who did receive monetary aid from parents and grandparents to buy a house, 45% of Americans said they would not have been able to purchase a house without financial support from parents and grandparents.”

Bottom Line

Your equity could be the thing that makes homeownership possible for your children when they might not be able to do it on their own. So, here’s the question.

If helping your kids buy a home was more feasible than you thought, would you want to explore that option?

If you want to learn more or find out the best way to make it happen, talk to your lender and a financial advisor you trust.

To view original article, visit Keeping Current Matters.

Selling a Luxury House? Here’s Why Now Is a Good Time

High-end buyers tend to feel less of the affordability pressure weighing on many households today, so they keep buying even when the wider market slows.

More Homes, Better Prices: A Buyer’s Summer

Sellers are reading market conditions and are pricing accordingly from the start rather than listing high and cutting later, and buyers are taking note and making bids.

The “Take It or Leave It” Attitude Is Fading from the Market – What That Means for You

That’s why whether you’re buying or selling today, there are two terms you’ll hear a lot: concession and incentive.

What Buying or Selling a Home Gives Back to Your Community

Want to know what a move would mean where you live? A local agent can show you the figure close to home.

The 1 Factor That Explains Everything Happening with Home Prices Right Now

The national average of 1.7% price growth is accurate, but it’s an average of two very different stories happening at the same time – the few areas experiencing mild declines and the overwhelming majority that are still seeing prices rise.

That House That’s Been Sitting Could Be Your Best Shot at a Deal

A local agent has the context to tell which homes are the real opportunities and which are skippable.